ARIMA

Basic Overview

|

Description |

Forecasting function based on the autoregressive integrated moving average (ARIMA) model. More |

|

Signature |

ARIMA('Node', p, d, q, P, D, Q, m) |

|

Parameters |

|

|

Available from |

3.6.0

|

Example

Input: Data from 2000-2011 (Passenger historic.xlsx)

|

Year |

Month |

MEASURE |

|---|---|---|

|

2000 |

2000-01 |

112 |

|

... |

... |

... |

|

2011 |

2011-12 |

432 |

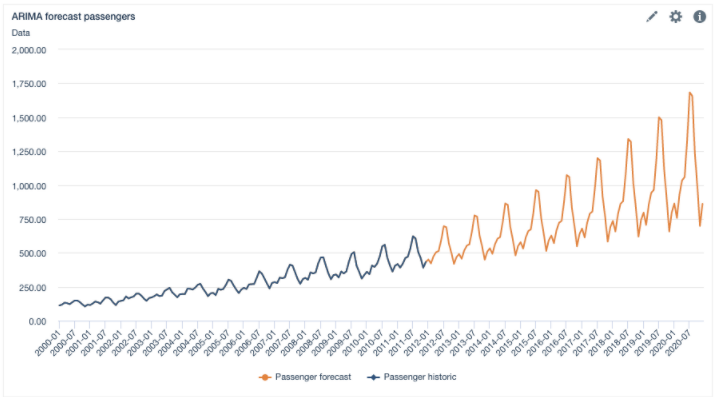

Output: ARIMA('Passenger historic', 1, 1, 1, 1, 0, 1, 12)

Data from 2000-2020

|

Year |

Month |

MEASURE |

|---|---|---|

|

2000 |

2000-01 |

112 |

|

... |

... |

... |

|

2011 |

2011-12 |

432 |

|

2012 |

2012-01 |

450 |

|

... |

... |

... |

|

2020 |

2020-12 |

861 |

Chart: